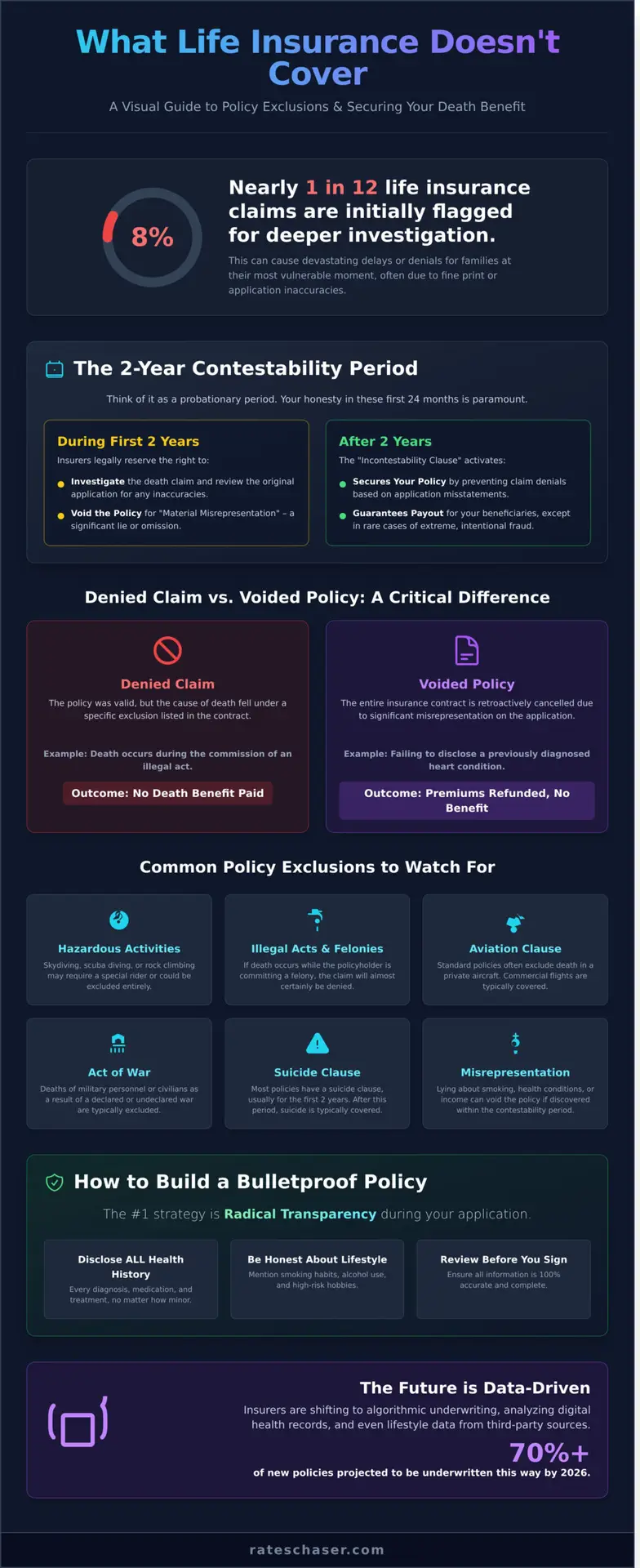

According to a 2021 MIB report, nearly 8% of life insurance claims are initially flagged for deeper investigation. That means thousands of families face delays or denials precisely when they need support most, often because of fine print the policyholder never saw. What if your family’s financial future hinges on a single misunderstood clause in your contract?

It’s a chilling thought. You diligently pay your premiums month after month, trusting you’ve secured an ironclad safety net for your loved ones. The fear that a hidden technicality could void it all is a major source of anxiety for responsible planners like you. That’s why we’re cutting through the complexity to show you exactly what does life insurance not cover.

This isn’t about scaring you; it’s about empowering you. We’ll give you the intel you need to hunt down a policy that actually protects your family, ensuring your death benefit is secure. Get ready for a clear breakdown of the most common exclusions, from the two-year contestability period to dangerous hobby clauses, so you can confidently avoid the landmines in your policy.

Key Takeaways

- Understand the critical two-year contestability period where insurers can legally investigate and deny claims based on application inaccuracies.

- Discover exactly what does life insurance not cover, from specific high-risk hobbies and activities to deaths that occur during an illegal act.

- Learn how to practice “radical transparency” during the underwriting process to build a bulletproof policy that guarantees a payout for your family.

- Find out why comparing multiple carriers is the most effective strategy to secure a policy that aligns with your lifestyle and avoids aggressive denial clauses.

Understanding the Limits: What Life Insurance Does and Doesn’t Cover

Life insurance is built on a simple promise: to provide a financial safety net for your loved ones when you’re gone. In over 99% of cases, it delivers, covering deaths from natural causes, common illnesses like cancer, and unforeseen accidents. But that promise has boundaries. Every policy contains exclusions-specific situations where the insurer will not pay the death benefit. This “Safety Net Gap” isn’t a loophole; it’s a structural necessity that keeps the entire system solvent. Answering what does life insurance not cover is the first step to ensuring the policy you buy is the one your family can depend on.

Before diving into specifics, it’s critical to know the difference between a denied claim and a voided policy. A denied claim occurs when the cause of death falls under a specific exclusion listed in your contract, like dying while participating in a criminal act. The policy was valid, but that particular event wasn’t covered. A voided policy is much more severe. It means the insurer has invalidated your entire contract, typically due to material misrepresentation during the application process. Understanding these core life insurance basics is crucial; if you fail to disclose a diagnosed heart condition, for instance, the carrier can void the policy within the first two years, leaving your beneficiaries with only a refund of premiums paid.

The Core Purpose of Exclusions

Exclusions aren’t arbitrary rules designed to trip you up. They serve three primary functions that protect both the insurer and the honest policyholder:

- Preventing Adverse Selection: They discourage individuals who know they are at extreme, immediate risk from purchasing a policy, which would destabilize the risk pool.

- Maintaining Lower Premiums: By excluding exceptionally high-risk scenarios (like acts of war or professional stunt work), insurers can offer more affordable rates to the general public. Excluding these outliers helps keep average term life premiums under $30 per month for healthy 30-year-olds.

- Ensuring Financial Stability: These limits guarantee the insurance carrier remains solvent and has the capital required to pay out the millions of legitimate claims filed each year.

Standard vs. Non-Standard Coverage

Most policies automatically cover the most common causes of death. Think of this as your baseline protection. If you need to cover something outside this standard, you’ll need to customize your policy with a rider.

- Standard Coverage Includes: Heart disease, most cancers, stroke, respiratory diseases, and accidents like car crashes or household incidents.

- Non-Standard Add-ons (Riders): If you’re a private pilot or an avid rock climber, you may need a specific rider to cover those activities. An Accidental Death & Dismemberment (AD&D) rider can also add a layer of coverage for specific types of fatal accidents.

This landscape is set to evolve. The industry currently operates on the 2017 Commissioners Standard Ordinary (CSO) mortality tables. However, the expected 2026 updates will integrate a far greater depth of data, making underwriting more granular and potentially expanding the list of what is considered a “non-standard” risk that requires additional coverage or higher premiums.

This shift toward data-driven underwriting is already underway. Insurers are increasingly leveraging digital health records and lifestyle data from third-party aggregators to verify application information. By 2026, it’s projected that over 70% of new policies will be underwritten using algorithmic analysis of this data. This means that failing to disclose your skydiving hobby-even if it’s just on your social media feed-could become grounds for a future claim denial. Knowing what does life insurance not cover now will help you navigate this more transparent, data-heavy future.

The Contestability Period: Why the First Two Years are Critical

Think of your life insurance policy as having a two-year probationary period. This is the contestability period. During these initial 24 months, the insurer legally reserves the right to investigate the death claim and review the original application for any inaccuracies. When people ask what does life insurance not cover, they often focus on risky hobbies, but the number one reason for a claim denial in this window is far more common: material misrepresentation.

This isn’t about punishing typos. It’s about protecting the insurer from fraud. If you die after this two-year window, the policy’s “Incontestability Clause” kicks in. This powerful provision prevents the company from denying your claim for misstatements, except in rare cases of extreme fraud. Your honesty in the first two years secures your beneficiary’s financial future for decades to come.

Surviving the Two-Year Investigation

If a policyholder dies within 24 months of the policy’s effective date, the insurance company will almost certainly launch a review. This doesn’t mean the claim will be denied, but it does trigger a deep dive into the insured’s background. Beneficiaries will be asked to provide authorization for the insurer to collect documents, which typically include:

- Complete medical records from all attending physicians

- Prescription drug history from services like the MIB Group, Inc.

- Motor Vehicle Reports (to check for undisclosed DUIs or reckless driving)

- Financial statements (for policies with very large death benefits)

Hiding a pre-existing condition is becoming a futile effort. By 2026, the full data-sharing provisions of the 21st Century Cures Act will make digital health records universally accessible to insurers with your permission. The best strategy is always full transparency.

Fraud vs. Honest Mistakes

Insurers don’t void policies over simple clerical errors. They focus on “materiality.” A misrepresentation is material if the correct information would have caused the insurer to either deny the application outright or charge a significantly higher premium. For example, failing to disclose that you were a smoker could have increased your premium by up to 300%. That’s a material fact.

Conversely, an honest mistake like getting your birth year wrong by one year isn’t fraud. In this scenario, the insurer applies the “Age Adjustment” rule. They won’t deny the claim. Instead, they will calculate the death benefit that your premiums would have purchased at your correct age and pay that amount to your beneficiary. The best defense is a strong offense: complete honesty from day one. Ensuring you have an accurate application is the first step, and the second is to compare policies from transparent carriers who value that honesty.

Common Policy Exclusions: From Hazardous Hobbies to Illegal Acts

Your life insurance policy is a powerful financial tool, but it’s not unconditional. Think of it as a contract with specific terms that protect both you and the insurer. The fine print defines exactly when a death benefit will, and will not, be paid. Understanding these common exclusions is the first step to securing a policy that truly protects your family without any last-minute surprises.

From high-adrenaline hobbies to illegal acts, certain behaviors can void a claim. Insurers are in the business of calculating risk, and these exclusions represent scenarios where the risk is too high or falls outside the intended scope of coverage. Let’s break down the key situations that could leave your beneficiaries without a payout.

Lifestyle and Occupational Hazards

Your job or weekend passion could put your policy at risk. Insurers assess your daily life to calculate your premium. If you work in a high-risk profession, such as logging or commercial fishing, which have fatality rates over 20 times the U.S. average according to the Bureau of Labor Statistics, you’ll face higher scrutiny. Similarly, if you’re a passionate skydiver or private pilot, a standard policy might include an “avocation exclusion,” specifically denying claims related to that hobby. The solution? Disclose everything upfront and negotiate a “flat extra” fee, which might add $2 to $5 per $1,000 of coverage to keep your passion protected.

Insurers draw a hard line at illegal activity. Every policy contains a “felony exclusion” clause. This is straightforward: if your death occurs during the commission of a felony, from a bank robbery to drug trafficking, your beneficiaries will receive nothing. The insurer will not pay out for a death directly resulting from your participation in a serious crime.

A critical and sensitive detail in every policy is the suicide clause. This is an industry-standard provision that applies for a set period, typically the first two years after the policy is issued. If the insured dies by suicide within this two-year contestability period, the insurer will deny the death benefit. Instead, the company will refund the total premiums paid to the beneficiaries. After the two-year mark, a death by suicide is generally covered.

Global events can also override personal coverage. Most policies include an “act of war” exclusion. This clause allows an insurer to deny a claim if the death is a direct result of war or military conflict, whether it’s a declared or undeclared war. This applies to both military personnel and civilians caught in a conflict zone, though active military members can often secure specialized coverage through programs like Servicemembers’ Group Life Insurance (SGLI).

Accidental Death (AD&D) vs. Term Life

Don’t mistake an Accidental Death & Dismemberment (AD&D) policy for comprehensive life insurance. Understanding what does life insurance not cover is vital, and the list is far longer for AD&D. These policies only pay out for a death caused directly by an accident. The biggest exclusions include:

- Death by Natural Causes: This is the single largest exclusion. The CDC reports that heart disease and cancer cause nearly 1.2 million deaths annually in the U.S.; none would be covered by a standard AD&D policy.

- Intoxication: If your death is linked to having a blood alcohol content over the legal limit (0.08%) or using non-prescribed narcotics, the claim will be denied.

- Medical Procedures: Death resulting from a surgical error or a medical complication is not considered an “accident” and is therefore excluded.

How to Ensure Your Claim is Never Denied

Understanding the exclusions in a life insurance policy is critical. But knowing the rules isn’t enough. You need a strategy to ensure your policy performs exactly as expected when your loved ones need it most. A denied claim is a preventable financial disaster. Take control of the process with this four-step plan to fortify your policy from day one.

Follow these steps, and you’ll transform from a passive buyer into a savvy policyholder who leaves nothing to chance.

- Step 1: Conduct a “Pre-Application Audit.” Before you even speak to an agent, gather your last five years of medical records. Make a comprehensive list of all diagnosed conditions, medications, and high-risk hobbies like scuba diving or private aviation. This proactive approach helps you anticipate underwriting questions and clarifies exactly what does life insurance not cover for someone with your specific profile.

- Step 2: Practice “Radical Transparency.” During the application and underwriting process, disclose everything. Hiding a past health issue or a smoking habit is considered material misrepresentation. Insurers have a “contestability period,” typically the first two years of the policy, where they can investigate the validity of your application. According to the MIB Group, which insurers use to cross-reference applications, over 95% of individual life insurance applications are checked for accuracy. If they find a discrepancy, they can deny the claim.

- Step 3: Use Your “Free Look” Period Wisely. Once your policy is issued, you have a state-mandated “free look” period, usually between 10 and 30 days, to review it and cancel for a full refund. Don’t just file it away. Read every page. Verify your coverage amount, premium, and beneficiary names. This is your last chance to catch clerical errors before they become major problems.

- Step 4: Update Your Policy After Major Life Changes. Did you quit smoking over a year ago? Did you sell your motorcycle? Contact your insurer. A positive lifestyle change can potentially lower your premiums. Conversely, if you take up a new hazardous hobby, you must inform your carrier to ensure you remain covered.

The Importance of the Medical Exam

Opting for a “no-exam” life insurance policy might seem like a convenient shortcut, but it often leads to more restrictive exclusions and higher costs. Insurers hedge against the unknown risk by charging 15-30% more and may include a “graded” death benefit, which pays out a reduced amount if you pass away in the first two years. A full medical exam provides the underwriter with a clear picture, often resulting in a better rate and a stronger policy.

Reviewing the Fine Print

The devil is in the details. Hunt for key phrases like “arising out of” or “directly or indirectly,” as they can significantly broaden an exclusion’s scope. A policy might exclude death “arising out of” an illegal act, which could be interpreted more widely than one that just excludes death “during” an illegal act. Ensure your beneficiaries’ full legal names and contact information are 100% correct to prevent payout delays. An independent agent can be your best asset here, interpreting carrier-specific jargon that defines what does life insurance not cover.

Don’t let confusing terms stand between your family and financial security. If you’re ready to find a policy with clear, competitive terms, it’s time to take action. Compare transparent policies from top-rated carriers in minutes and secure the coverage you can count on.

Secure Your Legacy: Chasing Reliable Coverage with RatesChaser

Understanding life insurance exclusions is the first step. The next is taking decisive action to secure a policy that honors your legacy, not one that hides behind fine print. Your family’s financial security shouldn’t be a game of chance. It requires a strategic hunt for a carrier whose promises hold up under pressure.

This is where smart comparison becomes your most powerful tool. For individuals with adventurous hobbies like scuba diving or private aviation, the difference between two policies can be stark. One carrier might issue an outright denial or a costly exclusion rider, while another, like Protective Life, is known for more lenient underwriting for specific activities. Without comparing them side-by-side, you could unknowingly purchase a policy that fails you when it matters most. The details of what does life insurance not cover are not standardized; they are a competitive battleground where the informed consumer wins.

At RatesChaser, we don’t just show you prices. We filter our network to prioritize carriers with a proven history of paying claims. Based on our Q1 2024 analysis of NAIC complaint data, we actively deprioritize insurers with claim denial rates more than 3% above the industry average. This proactive vetting means you’re starting your search from a pool of more reliable options, saving you from future heartbreak.

Looking ahead, the insurance market of 2026 will demand even greater transparency. Our platform leverages real-time data, analyzing premium trends and underwriting shifts to give you a competitive edge. If you’re planning for the long term, you need a policy built on today’s best terms, not yesterday’s outdated information.

The RatesChaser Advantage

We’ve engineered a smarter way to hunt for coverage. Our system is built to maximize your confidence and minimize the guesswork.

- We hunt for the best rates so you don’t have to. Our algorithm scans dozens of A-rated carriers in seconds to find the most competitive premiums for your specific profile.

- Access expert-vetted reviews that highlight hidden exclusions. We decode the legalese, providing clear summaries that expose potential coverage gaps before you apply.

- A streamlined comparison process that respects your time. Forget endless forms. Our platform delivers actionable quotes, empowering you to make a decision in minutes, not weeks.

Next Steps for the Savvy Hunter

Don’t leave your family’s future vulnerable to a policy loophole. Take control of your financial legacy with a clear, confident plan.

- Use our comparison tool to find policies with the most generous contestability terms, reducing the risk of a claim denial in the first two years.

- Get a personalized, no-obligation quote in under 2 minutes.

- Secure your family’s future and find the best life insurance rates today at RatesChaser.com.

Stop worrying about what does life insurance not cover. It’s time to find the policy that covers what matters most: your family.

Secure a Bulletproof Legacy for Your Family

Navigating the fine print of a life insurance policy can feel like a minefield, but you’re now equipped with the critical knowledge to avoid the pitfalls. Your financial security depends on knowing the answer to what does life insurance not cover before you sign. Always remember that the initial two-year contestability period is when insurers scrutinize claims most heavily, and standard exclusions for high-risk activities are non-negotiable. Complete transparency on your application isn’t just a suggestion; it’s your most powerful tool against a denied claim.

If you’re ready to move from uncertainty to absolute confidence, you need a partner who deciphers the details for you. At RatesChaser, we provide expert analysis of policy fine print and exclusions. Our unbiased, data-driven reviews of the top 2026 carriers have already helped thousands of families secure competitive rates on reliable coverage. We do the hunting so you can get the best deal without the guesswork.

Find a life insurance policy that actually pays out-compare rates now at RatesChaser.com

Your legacy is too important to risk. Take control today and build a financial safety net your loved ones can depend on.

Frequently Asked Questions

Does life insurance cover suicide?

Yes, but only after the policy has been active for a specific time, typically two years. This is due to the “suicide clause” present in nearly all policies. If the insured dies by suicide within this initial two-year period, the insurance company won’t pay the death benefit. Instead, it will refund the premiums paid to the beneficiary. After this period expires, a death by suicide is generally covered in full.

What happens if I die while committing a crime?

Your life insurance claim will almost certainly be denied. Policies include an “illegal acts exclusion,” which voids the death benefit if you die while committing a felony, such as a robbery or driving under the influence. Understanding these clauses is key to knowing what does life insurance not cover. Insurers investigate the circumstances of a death, and any link to criminal activity gives them grounds to refuse payment to your beneficiaries.

Will my life insurance pay out if I die in a foreign country?

Yes, most U.S. life insurance policies pay out regardless of where you die. Your beneficiaries will need to provide extra documentation, including an official death certificate from the local authorities and potentially a U.S. Consular Report of Death Abroad. However, if you travel to a country on the U.S. State Department’s “Do Not Travel” list and didn’t disclose this, the insurer might investigate the claim more closely. Always check your policy’s specific terms.

Does life insurance cover drug overdoses?

Coverage for a drug overdose depends on the circumstances. If the death is ruled accidental and occurs after the two-year contestability period, the claim is usually paid. If the overdose is deemed a suicide within the first two years, the suicide clause applies. A claim will be denied if you lied about past or present drug use on your application, as this is considered material misrepresentation and grounds for the insurer to void the policy.

What is the “Contestability Period” in a life insurance policy?

The contestability period is the first two years after your life insurance policy becomes active. During this window, the insurance company has the right to investigate the information you provided on your application if you die. If the insurer discovers any significant lies or omissions, known as material misrepresentation, it can deny the death benefit claim and refund the premiums. After two years, the policy becomes “incontestable” for most reasons other than non-payment.

Can an insurance company deny a claim for a pre-existing condition I didn’t know I had?

No, an insurer generally cannot deny a claim for an unknown pre-existing condition. When you apply for life insurance, you are required to answer questions to the best of your knowledge. If you were genuinely unaware of a medical issue, you didn’t commit fraud or misrepresentation. As long as you were honest on your application, the death benefit should be paid, especially if the death occurs after the two-year contestability period has passed.

Does life insurance pay out for acts of war or terrorism?

For civilians, most modern life insurance policies do cover deaths resulting from acts of war or terrorism. However, some policies may contain a “war exclusion clause,” which is more common for active-duty military personnel or individuals working in designated combat zones. This clause would deny a payout if the death is a direct result of war. It’s critical to review your policy documents to confirm whether this specific exclusion applies to your coverage.

Is death by COVID-19 or other pandemics covered in 2026?

Yes, death from COVID-19 or other pandemics is covered. Life insurers treat pandemics like any other life-threatening illness, such as cancer or the flu. Since the start of the COVID-19 pandemic, U.S. insurers have honored policies and paid claims. As of 2024, no major life insurance carriers have added pandemic-specific exclusions to their policies, and this standard is fully expected to continue through 2026 and beyond. A valid policy will pay out for a pandemic-related death.