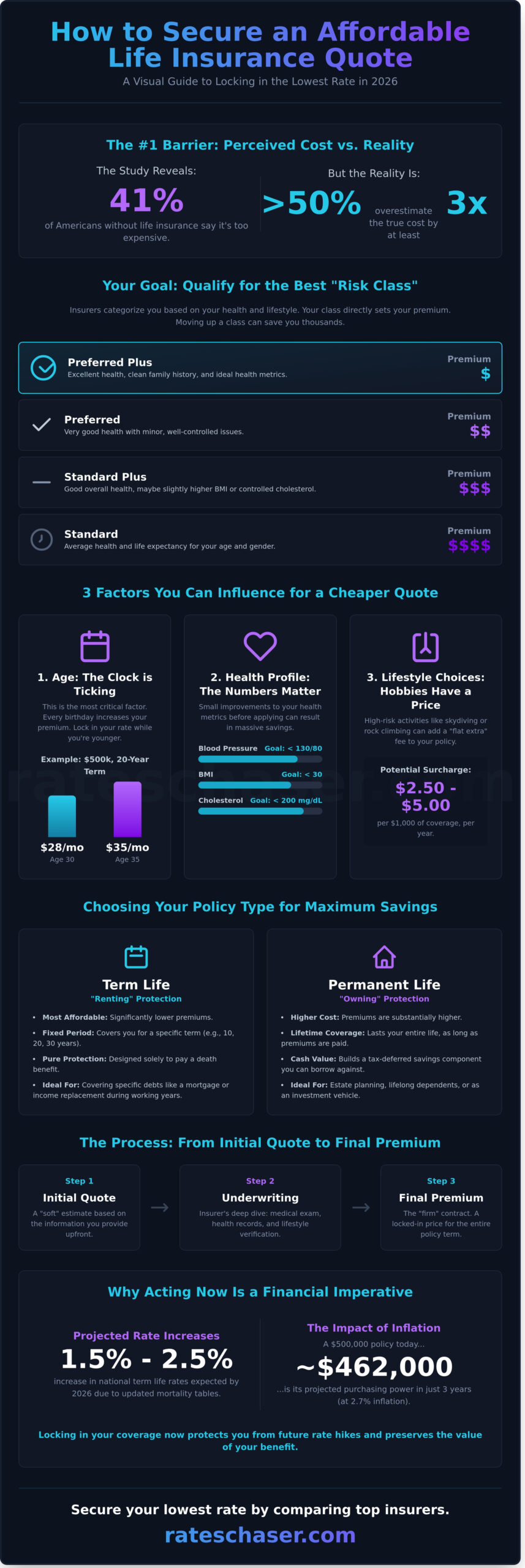

According to the 2023 LIMRA Insurance Barometer Study, 41% of Americans without life insurance say it’s too expensive. Yet, the same study reveals that more than half of them overestimate the actual cost by at least three times. What if you could secure a policy for less than your monthly streaming subscriptions?

It’s a common fear. You see the ads, you hear the confusing jargon about term versus whole life, and you worry that a single health question will send your premiums skyrocketing. The entire process can feel designed to make you overpay. It doesn’t have to be this way. This guide delivers the exact playbook on how to get an affordable life insurance quote in 2026. You will learn the strategies to optimize your risk profile, decode policy structures, and lock in the lowest possible rate without sacrificing coverage.

Get ready for a three-step hunt: first, we’ll sharpen your application to present you as a low-risk candidate; next, we’ll compare the right policies for your budget; and finally, we’ll show you how to use modern tools to make insurers compete for your business.

Key Takeaways

- Unlock lower premiums by understanding how insurers evaluate your health and assign you to a specific “Risk Class.”

- Discover why acting now is critical and how to choose between Term and Permanent policies to maximize your savings from day one.

- Learn exactly how to get an affordable life insurance quote by strategically preparing your health profile before you start comparing carriers.

- Master a step-by-step optimization plan to compare top-rated insurers, ensuring you secure the best possible coverage without overpaying.

Understanding Life Insurance Quote Variables: Why Rates Differ

The first step in understanding how to get an affordable life insurance quote is recognizing that it’s a personalized estimate, not a one-size-fits-all price tag. Think of a quote as an insurer’s initial assessment of your risk profile. They use complex mathematical models to predict longevity, and your quote reflects where you fall on that spectrum. This is why two 45-year-olds can receive dramatically different rates; one might be a non-smoking marathon runner, while the other manages high blood pressure.

Insurers categorize applicants into “Risk Classes” to streamline this process. Your assigned class directly determines your premium. While the names vary slightly between companies, they generally include:

- Preferred Plus: Reserved for individuals in excellent health with a clean family medical history. This class secures the lowest possible rates.

- Preferred: For those in very good health with only minor, well-controlled health issues.

- Standard Plus: You’re in good health overall but may have a slightly higher BMI or controlled cholesterol.

- Standard: Represents average health and life expectancy for your age and gender.

- Substandard (Table Ratings): Applicants with significant health conditions or high-risk hobbies fall into this category, with premiums adjusted accordingly.

Your goal is to qualify for the best risk class possible. Every factor, from your driving record to your cholesterol levels, is a piece of the puzzle that insurers use to build your profile and calculate your rate.

The Role of Actuarial Risk in Pricing

Insurance isn’t a guess; it’s a science. Actuaries analyze millions of data points to calculate the probability of a claim. For a comprehensive overview of life insurance as a financial tool, you can see how this risk assessment has evolved over centuries. Looking ahead, industry analysts project a modest 1.5% to 2.5% increase in national term life rates by 2026, driven by updated mortality tables. It’s also crucial to consider inflation. A $500,000 death benefit secured today will have the purchasing power of approximately $462,000 in just three years, assuming a 2.7% annual inflation rate, making it vital to choose a coverage amount that accounts for future costs.

Quote vs. Premium: Knowing the Difference

An initial quote is the “soft” invitation, while the final premium is the “firm” contract. Your quote is based on the information you provide upfront. The premium is the final, locked-in price determined after the underwriting process, which often includes a medical exam and a review of your health records. If the medical review uncovers information that changes your risk profile, your final premium may be higher than your initial quote. This transparency is key to finding a policy you can trust. A level premium is your key to long-term affordability, locking in your rate for the entire term of the policy.

5 Critical Factors That Secure an Affordable Life Insurance Quote

Life insurance underwriters are risk analysts. Their primary job is to predict your longevity, and your premium is the price of that prediction. Your job is to present the lowest-risk profile possible. Understanding how to get an affordable life insurance quote means controlling the variables you can and acting decisively on the ones you can’t. Let’s break down the five factors that dictate your final rate.

1. Age: This is the most critical, non-negotiable factor. Every birthday you celebrate increases your premium. Insurers use your “insurance age,” which is often your age at your nearest birthday. Waiting just six months could push you into a new price bracket, costing you thousands over the policy’s term. A 30-year-old male might secure a $500,000, 20-year term policy for around $28 per month. That same policy for a 35-year-old jumps to nearly $35. Lock in your rate now; don’t pay more later.

2. Health Profile: Your current health is a direct indicator of risk. Underwriters analyze key metrics to assign you a risk class, such as “Preferred Plus,” “Standard,” or “Substandard.” Each step down can increase your premium by 25% or more. They focus on:

- Body Mass Index (BMI): Insurers typically require a BMI under 30 for the best rates.

- Blood Pressure: A reading below 130/80 is the gold standard for top-tier pricing.

- Cholesterol: A total cholesterol level under 200 mg/dL with a healthy HDL ratio is the target.

3. Lifestyle Choices: What you do for fun and how you live your life matters. Insurers will check for high-risk activities. A passion for skydiving or rock climbing can add a “flat extra” fee of $2.50 to $5.00 per $1,000 of coverage. Your driving record is also under review; a DUI within the last five years can lead to an automatic decline from many top carriers.

4. Policy Duration: The length of your term has a massive impact on cost. A 10-year term policy is designed to cover short-term debts and is significantly cheaper because the insurer’s risk is lower. A 30-year term, which might cover a full mortgage, can cost two to three times more per month. If you need coverage for 25 years, don’t automatically buy a 30-year policy. Compare the cost of a 25-year term to trim the expense.

5. Coverage Amount: Finding the “sweet spot” is key. You need enough coverage to protect your family, but over-insuring wastes money. Surprisingly, a $1 million policy isn’t double the price of a $500,000 one. Insurers offer price breaks at certain thresholds, so the cost-per-thousand of coverage often drops as the face amount increases. Comparing these variables is how you can unlock the most competitive rates for your specific needs. Mastering these factors is central to finding a policy that fits your budget; for a deeper dive, you can find more affordable life insurance tips from industry experts.

Health Optimization Before the Medical Exam

If your policy requires a medical exam, you can take simple steps to improve your results. In the 24 hours prior, avoid caffeine, alcohol, and high-sodium foods that can temporarily spike your blood pressure. Get a full eight hours of sleep. If you have a managed condition like hypertension, provide documentation from your doctor showing consistent treatment and stable readings to the underwriter. For those concerned about what an exam might reveal, a “no-exam” policy can offer a faster path to coverage.

The Smoking Penalty and How to Avoid It

Using nicotine is the single most expensive factor you can control. Insurers charge smokers anywhere from 200% to 400% more than non-smokers. To qualify for non-smoker rates, you must be completely nicotine-free for at least 12 months, with some carriers requiring 24 months for the best rates. By 2026, nearly all top insurers will treat vaping and other nicotine products like e-cigarettes or patches exactly the same as traditional cigarettes, so quitting all forms is the only path to major savings.

Comparing Policy Types: Term vs. Permanent for Maximum Savings

To understand how to get an affordable life insurance quote, you must first understand the product you’re buying. At its core, the legal definition of life insurance describes a contract that pays a benefit upon death. How that contract is structured determines its cost. The market presents two primary paths: Term and Permanent. Your choice here is the single biggest factor affecting your quote.

Term Life Insurance is pure protection. You buy coverage for a specific period, typically 10, 20, or 30 years. If you pass away during that term, your beneficiaries receive the death benefit. If you don’t, the policy expires. It’s simple, straightforward, and by far the most affordable option for the vast majority of families. Think of it as renting protection for the years you need it most.

Permanent Life Insurance, like Whole Life or Universal Life, is designed to last your entire life. It combines a death benefit with a cash value savings component that grows over time. This dual function makes premiums 5 to 15 times higher than a comparable term policy. If you have complex estate planning needs or want to leave a guaranteed inheritance, it can be a fit. For everyone else, it’s an expensive tool for a job that can be done more efficiently.

This leads to the “Buy Term and Invest the Difference” (BTID) philosophy. A savvy hunter secures a low-cost term policy and invests the money saved on premiums into their own retirement accounts, like a 401(k) or Roth IRA. You get the protection you need and control your investment growth, often yielding better long-term results.

Finally, watch for riders. These are policy add-ons that customize your coverage. A Waiver of Premium rider, for instance, covers your payments if you become disabled. While useful, each rider adds to your monthly cost. Analyze them carefully to ensure you’re only paying for what you truly need.

The Laddering Strategy: Cutting Costs by Stacking Policies

Why pay for maximum coverage when your financial needs are declining? The laddering strategy lets you “hunt” for savings by stacking multiple smaller term policies with different end dates. This aligns your coverage precisely with your debts. For example, a 35-year-old needing $1 million of coverage for 30 years could buy one massive policy for about $78/month. Or, they could ladder:

- Policy 1: $500,000 for 30 years (to cover the mortgage)

- Policy 2: $300,000 for 20 years (until kids are through college)

- Policy 3: $200,000 for 10 years (for the highest-earning years)

This approach drops your total coverage-and your premium-as your major financial obligations disappear over time, potentially saving you thousands over the life of your policies.

When “Cheap” Becomes Expensive: Avoiding Under-Insurance

The quest for an affordable life insurance quote can be a trap if it leads to inadequate coverage. A $250,000 policy is cheap, but it’s dangerously expensive if your family truly needs $1 million to replace your income and pay off a mortgage. The hidden cost of under-insurance is your family’s financial security.

Don’t rely solely on “Group Life” from your employer. It’s a great perk, but it’s rarely enough, often capping at 1-2x your salary. Plus, you usually lose it if you leave the job. The smartest move is to calculate your actual need. Use a comprehensive Life Insurance Needs Calculator to find your number, then hunt for a policy that truly secures your family’s future.

How to Secure Your Quote: A Step-by-Step Optimization Plan

You’ve done the prep work. Now it’s time to execute. Securing the best possible rate isn’t about luck; it’s about running a smart, strategic process. This plan transforms you from a passive applicant into an active hunter, equipped to find the market’s most competitive offers. Following these steps is fundamental to understanding how to get an affordable life insurance quote that doesn’t compromise on quality.

First, arm yourself with data. Before you fill out a single form, gather your complete medical history, including dates of diagnoses, physician contact information, and a list of current prescriptions. Insurers will also ask about your immediate family’s health history (parents and siblings), specifically for conditions like cancer or heart disease diagnosed before age 60. Having this information ready prevents delays and ensures your application is accurate from the start.

Next, define your financial target with precision. Separate your coverage needs into two categories:

- Must-Haves: This is your non-negotiable safety net. It should cover your mortgage balance, all outstanding debts, and income replacement for at least 10 years.

- Nice-to-Haves: This includes legacy goals, like funding a child’s college education or leaving a larger tax-free inheritance.

If your budget is tight, lock in the “Must-Haves” first. You can often add more coverage later.

Navigating the Online Quote Process

Accuracy is your greatest asset. While it might be tempting to omit certain details, insurers have sophisticated verification systems. Lying about tobacco use, a DUI conviction within the last 10 years, or a major medical diagnosis is a guaranteed way to have a future claim denied. The MIB (Medical Information Bureau) cross-references data from nearly every life insurance application submitted in the U.S., flagging inconsistencies for underwriters. Be prepared for follow-up questions; they are a sign an underwriter is actively working on your file.

Finalizing the Best Deal

Once quotes arrive, your analysis begins. Look past the headline premium and examine the illustration’s fine print, paying close attention to the “guaranteed” versus “non-guaranteed” columns. Then, confirm your policy includes a “Free Look” period. This is a state-mandated window, typically 10 to 30 days, allowing you to cancel the policy for a full refund with no questions asked. Finally, if you want to unlock an immediate discount, ask to pay your premium annually. This simple switch can reduce your total cost by up to 8% per year.

The single most effective strategy for how to get an affordable life insurance quote is to make top carriers compete for your business. By applying for several quotes at once, you create leverage and gain a clear view of the entire market. Ready to see how the top-rated insurers stack up for you?

Chasing the Best Rates: Why RatesChaser is Your Strategic Partner

You’ve done the research and defined your needs. Now it’s time to execute. The final step in securing financial protection for your family is often the most confusing: comparing dozens of competing offers. With hundreds of carriers, each with different underwriting rules and pricing models, how do you ensure you’re not overpaying? This is where a strategic partner transforms the game. RatesChaser isn’t just another comparison tool; we are your dedicated advocate in the financial jungle, built to hunt down maximum value and eliminate confusion.

We’ve engineered a system that bypasses the slow, frustrating process of calling individual agents. Our platform aggregates real-time data from over 40 of the nation’s top-rated life insurance carriers, presenting you with a clear, side-by-side comparison in minutes. This is our “Savvy Hunter” approach in action. It’s a blend of powerful technology and market intelligence. By analyzing thousands of data points, from your health profile to each carrier’s specific risk appetite, we pinpoint the most competitive premiums available. The result isn’t just convenience; it’s tangible savings. Our users save an average of 25% on their annual premiums compared to accepting the first quote they receive from a single provider.

Real-Time Market Monitoring

The insurance market is dynamic. Our technology constantly monitors rate changes across the US, ensuring the quotes you see for 2026 are accurate and competitive. We exclusively feature A-rated or better carriers from agencies like A.M. Best, guaranteeing long-term claim security for your loved ones. See our comprehensive breakdown in the Top Life Insurance Companies roundup.

The fundamental challenge of learning how to get an affordable life insurance quote is cutting through biased sales pitches. When you speak to a captive insurance agent, they work for their carrier, not for you. Their goal is to sell their company’s product, whether it’s the best fit or not. RatesChaser flips that model on its head. We provide a completely unbiased, third-party platform that puts you in the driver’s seat. We don’t favor one company over another; our system is designed for 100% transparency. Our mission is to present the hard data and empower you to make a confident decision without the sales pressure. You see the whole market, not just one corner of it.

Empowering Your Financial Future

Securing a life insurance policy is one of the most powerful financial moves you can make for your family. It’s a proactive win, a promise of security that transcends uncertainty. Remember the old saying: “The best time to buy was yesterday; the second best time is now.” Don’t wait for rates to rise. Take control of your financial legacy today.

The path to securing your family’s future is clear. You have the knowledge and the tools to make a smart, cost-effective decision. The next step is simple. Use our free comparison engine to see your personalized quotes from top carriers in under two minutes. Stop wondering if you’re getting a fair price and start saving.

Your Hunt for an Affordable Policy Ends Here

Securing financial protection for your loved ones in 2026 isn’t a game of chance; it’s a strategic hunt. The path to lower premiums is clear: you must understand the quote variables, optimize the 5 critical factors within your control, and choose the right policy type for your budget. For many, a term life policy offers the most direct route to maximum savings. Armed with this knowledge, you’ve moved beyond simply searching for a policy; you’re now equipped to engineer a better outcome. The question of how to get an affordable life insurance quote is no longer a mystery.

Now, it’s time to claim your advantage. Don’t let the best rates slip away by comparing options one by one. Secure your family’s future and compare life insurance quotes today at RatesChaser. Our no-obligation platform gives you a transparent, data-driven look at offers from 50+ A-rated carriers. With average user savings of $450 per year, the smartest move you can make is just one click away. Take control of your financial legacy.

Frequently Asked Questions

Is it better to get a life insurance quote online or through an agent?

Getting a quote online is faster and more efficient for comparing multiple offers. Digital platforms allow you to compare rates from over 15 top carriers in under 5 minutes, putting you in control of the process. If you have a complex health history or specialized financial needs, an agent can provide personalized guidance. For most people seeking straightforward term life coverage, online tools provide the quickest path to securing a competitive rate.

Can I get an affordable life insurance quote if I have a pre-existing condition?

Yes, you can absolutely secure a policy with a pre-existing condition. The key to understanding how to get an affordable life insurance quote is complete transparency about your health. For example, well-managed conditions like Type 2 diabetes or high blood pressure might only increase your premium by 25% to 50%. Insurers focus on how you manage your health, so comparing quotes from carriers specializing in high-risk policies is your best strategy.

How much life insurance do I actually need for it to be “worth it”?

A strong benchmark is to secure a death benefit that is 10 to 12 times your current annual income. This amount is designed to replace your lost earnings and support your family. You should also factor in major debts like your mortgage and future costs like college tuition, which averaged over $36,000 per year for private universities in 2023. Calculating these specific needs ensures your policy provides complete financial protection for your loved ones.

What is the cheapest type of life insurance available in 2026?

Term life insurance is consistently the most affordable option, a fact that will hold true in 2026. It provides pure death benefit protection for a specific period, such as 20 or 30 years, without building cash value. For perspective, a healthy 35-year-old can often secure a 20-year, $500,000 term policy for just $25-$35 per month. This is significantly less than whole life policies, which can cost 5 to 15 times more.

Will my life insurance quote change after the medical exam?

Yes, your final premium can change after the medical exam. Your initial quote is a non-binding estimate based on the information you provide. The exam results confirm your health classification. According to industry data from 2023, approximately 30% of applicants receive a final rate that differs from their initial quote. This is why complete honesty on your application from the start is the best strategy for receiving an accurate estimate.

How can I lower my life insurance premium after I’ve already bought a policy?

You can lower your premium by requesting a “re-rating” after making significant health improvements. If you’ve quit smoking for over 12 months, lost more than 10% of your body weight, or substantially improved your cholesterol levels, contact your insurer. Many companies will allow you to undergo a new medical exam after one to two years. A better health classification can directly unlock a lower monthly premium on your existing policy.

Do I need to get a new quote if I move to a different state?

No, your life insurance policy moves with you, so you don’t need to get a new quote or re-apply. Your coverage remains in force nationwide because it’s governed by the regulations of the state where it was originally issued. You just need to update your contact and billing address with your carrier to ensure there are no lapses in communication or payment. Your premium and death benefit will not change because of the move.

What happens if I lie on my life insurance quote application?

Lying on your application is fraud and can cause your policy to be canceled or a future claim to be denied. Insurers have a “contestability period,” which is the first two years of the policy. If you die during this time, the company will investigate your application. If they discover a material misrepresentation, like hiding a smoking habit or a medical diagnosis, they can legally deny the entire death benefit, leaving your beneficiaries with nothing.